Vietnam property knowledge

Financing a property purchase in Vietnam: payments, banks and currency

How do foreigners finance a property purchase in Vietnam?

How foreign buyers actually pay for a home in Hanoi

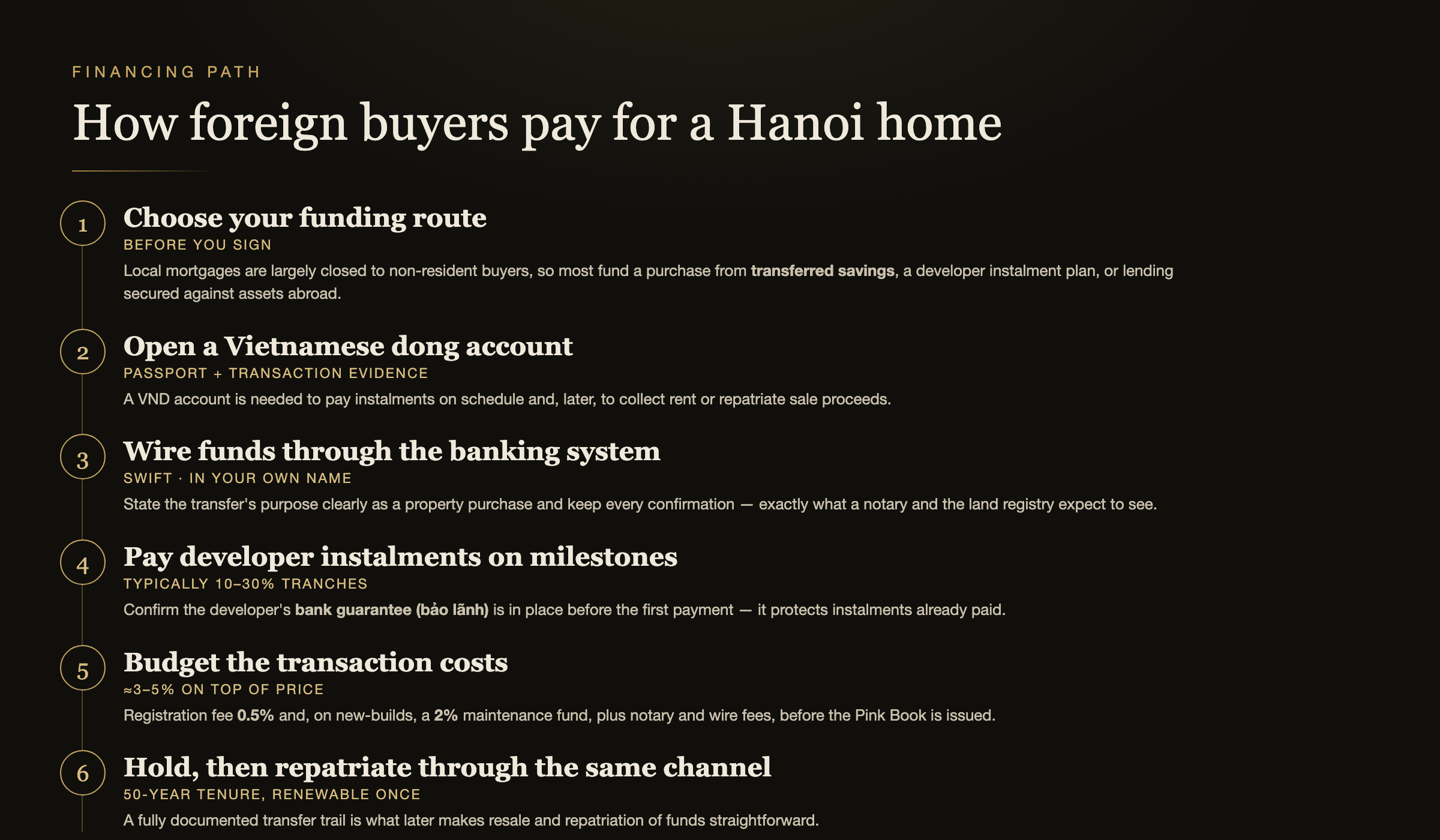

Updated July 2026. Because a Vietnamese mortgage is rarely on the table for a non-resident foreign buyer, financing a Hanoi purchase looks different from financing one at home. Most European buyers use one, or a combination, of three routes: transferred cash, a developer instalment schedule on an off-plan unit, or lending arranged and secured entirely outside Vietnam. Understanding which combination suits your situation — and lining up the paperwork early — saves weeks once you have found the right apartment.

Cash, transferred through the banking system

The most common route is straightforward: sell or draw down assets at home, then wire the funds to Vietnam in one or several instalments timed to the payment schedule in your sale and purchase agreement. This is also the cleanest route from a compliance standpoint — a documented transfer, in your own name, for a stated property purchase, is exactly what a receiving bank and, later, a land registration office expect to see.

Developer instalment plans, not a loan

On off-plan and new-build projects, developers routinely spread the price itself over a payment schedule tied to construction milestones — typically a reservation deposit, then several tranches of 10–30% as the building progresses, with a final balance at handover. This eases cash flow, but it is a commercial payment plan, not financing: there is no interest, no lender and no separate approval process, and every instalment should be protected by the developer's bank guarantee (bảo lãnh). Confirm the guarantee is in place, and with which bank, before your first payment.

Lending secured outside Vietnam

A small number of international private banks and specialist lenders will extend credit to a European buyer purchasing overseas, secured against a property, portfolio or deposit held in their home country — released to you as a lump sum you then transfer to Vietnam like any other cash purchase. This is foreign-domiciled lending, not a Vietnamese mortgage, and terms, minimum amounts and eligibility vary widely by institution; our guide to Foreign National loans for non-residents and our review of HSBC Expat's mortgage service set out how this works in practice.

Opening a bank account and moving money into Vietnam

Do you need a Vietnamese bank account?

In practice, yes. You will want a Vietnamese dong (VND) account to receive incoming transfers, pay instalments on schedule, and later collect rental income or sale proceeds without repeated cross-border fees. Non-resident foreigners can open one at most major banks with a valid passport and evidence of the transaction — requirements, minimum deposits and processing times vary noticeably by branch and by bank, so it is worth comparing two or three before your first visit.

Sending the money

Transfer funds by international bank wire (SWIFT) directly into your own account, never through informal money changers or a third party's account, however convenient it looks. State the purpose of the transfer clearly as a property purchase and keep every confirmation — this paper trail is what a bank, a notary or the land registration office may ask for, and it is what later lets you repatriate sale proceeds cleanly when you exit.

Currency and exchange rate risk

Contracts and the pink book are denominated in Vietnamese dong, so your euros are converted at some point — either by your own bank before the wire or by the receiving bank on arrival. Exchange spreads differ meaningfully between institutions, and on a six-figure transfer a single percentage point is a material sum; compare rates before committing, and consider splitting a large transfer into tranches aligned with your payment schedule to smooth out currency movements rather than converting everything on one day. See our guide to taxes and fees for how these costs stack up against the price of the property.

What financing your purchase costs, on top of the price

Worked example on a €530,000 apartment — the current Tây Hồ median (live data) — funded by a single international transfer.

| — | Min | Max | Base |

|---|---|---|---|

| Registration fee (lệ phí trước bạ)Issues the Pink Book (sổ hồng) | 0.5% | 0.5% | % of declared valueBuyer, at title registration |

| Maintenance / sinking fundHeld by the building management board | 2% | 2% | % of valueBuyer, new-builds only |

| International wire fee & FX spreadIndicative — compare 2–3 banks before a large transfer | €150 | €2,000+ | one-off, scales with amount sentBuyer, on each transfer |

| Notary & administrative feesScales with contract value | €150 | €600 | one-offBuyer, at signing |

| Independent legal review of contract & payment scheduleStrongly advised for foreign buyers | 0.5% | 1% | % of price (optional)Buyer, before signing |

| Total | ≈3% | ≈5% |

Example — €530,000 apartment (Tây Hồ median), paid via international transfer

- Registration fee 0.5%

- €2,650 (~73M VND)

- Maintenance fund 2%

- €10,600 (~292M VND)

- Wire fee & FX spread

- €450 (~12M VND)

- Notary & admin

- €400 (~11M VND)

- Σ

- ≈ €14,100 (~388M VND) · about 2.7% of price, before any optional legal review

Housing Law 2023 · Land Law 2024 · Decree 95/2024/ND-CP

Frequently asked questions

How much money do I need to buy a house in Vietnam?

Because most non-resident foreigners cannot access a Vietnamese mortgage, budget the full purchase price up front, plus roughly 3–5% for registration, the new-build maintenance fund, notary costs and bank transfer fees. The price itself varies widely by district and property type — check current medians before setting a budget — and off-plan purchases let you spread that price over instalments even though no loan is involved.

Can foreigners get a mortgage in Vietnam?

In practice, rarely. Vietnamese banks generally reserve mortgage lending for residents with local income and a long-term visa or residence card, which excludes most non-resident foreign buyers. A small number of international banks with a Vietnam or regional presence offer lending secured against assets held abroad, but that is foreign-domiciled financing, not a local Vietnamese mortgage.

Do I need a Vietnamese bank account to buy property?

You will generally need a Vietnamese dong account to receive incoming transfers, pay instalments and later collect rental income or sale proceeds. Non-resident foreigners can open one at most major banks with a valid passport and evidence of the transaction, though requirements and processing times vary by branch.

How do I transfer money to Vietnam to pay for a property?

Send funds by international bank wire (SWIFT) directly into your own Vietnamese account, never through informal money changers or a third party's account. Keep every transfer confirmation and state its purpose as a property purchase — this record is what later lets you repatriate sale proceeds and is often requested at Pink Book registration.

Should I pay in euros or Vietnamese dong?

Contracts and the Pink Book are denominated in Vietnamese dong, so your euros are converted at some point — either by your own bank before the wire or by the receiving bank on arrival. Compare the exchange spread across two or three banks before a large transfer; on a six-figure sum, a single percentage point of spread is a meaningful amount.

What happens if the developer misses a payment milestone?

This is exactly what a bank guarantee is designed to cover: reputable developers are required to hold one, and it lets you reclaim instalments already paid if the project fails to reach agreed milestones. Confirm the guarantee is in place, and with which bank, before you sign the sale and purchase agreement.

Can I use an international bank like HSBC Expat for financing?

A small number of international private banking arms serve European buyers purchasing in Vietnam, generally through lending secured against assets held outside the country rather than a local Vietnamese mortgage. Eligibility, minimum balances and documentation vary by institution — treat this as a foreign-currency loan against your home assets, not local financing.

Sources

- Housing Law 2023 (Law No. 27/2023/QH15) — governs residential title registration and the new-build maintenance fund.

- Land Law 2024 (Law No. 31/2024/QH15) — governs land-use rights and the registration fee due on transfer.

- Decree 95/2024/ND-CP — implementing decree detailing Housing Law 2023 procedures (no verified official English-language URL at time of writing).

- General Department of Taxation (Tổng cục Thuế) — the authority administering property-related tax obligations in Vietnam.

Plan your payment schedule with our Hanoi desk

Tell us your budget, funding source and target district, and our advisory desk will map out a realistic payment and transfer schedule — deposit, instalments, fees — within 24 hours, with no obligation and no outbound referral.